Making Tax Digital and basis periods

Over the past few years, you will no doubt have heard of Making Tax Digital (MTD) being talked about on the news, particularly at budget time. If your business is VAT registered, then you will undoubtedly be familiar with the term.

MTD is the government’s initiative to digitalise and streamline the tax system.

From 6th April 2026 MTD for income tax self-assessment (ITSA) will be mandatory for self-employed or landlord businesses with an income of more than £50,000 (this has changed as, previously it was set at £10,000). From April 2027 that will reduce to £30,000.

Why do I need to care about this now?

Well, even though the deadline seems too far away to worry about now, some changes are already being introduced from April 2023 in preparation for the 2026 deadline. For example, the rules governing basis period for self-employed accounts will change and may impact how much tax you pay and when it is paid.

What is a basis period?

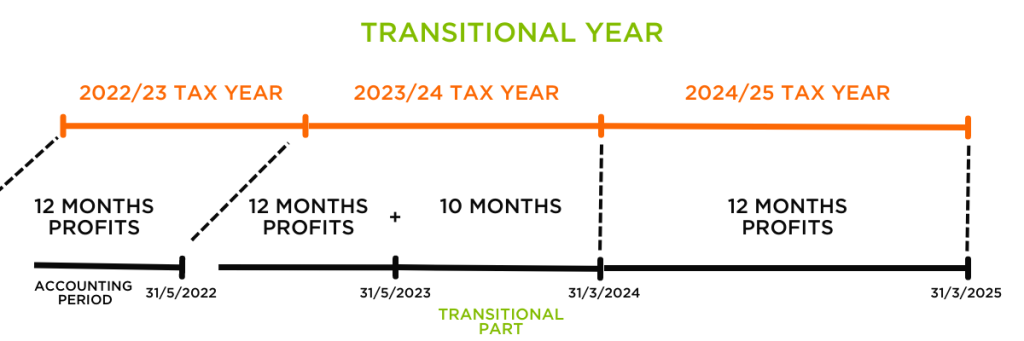

A basis period determines which profits are assessed in which tax year. Currently self-employed people are taxed on profits whose accounting year end falls within the tax year. This is called the current year basis. For example, if your accounts year end is 31/05/2021 then the profits for that period (1/6/2020 to 31/5/2021) are taxed on the 2021/22 tax year. This is because the 31/5/2021 falls between 6/4/2021 and 5/4/2022. Still confused? Here’s an illustration which shows how it currently works.

So, what is changing?

From the tax year, 2024/25 profits will be taxed based on the tax year (1 April to 31 March) for all self-employed and landlord businesses, regardless of your accounting year.

Why is it important to think about all this now?

It’s all about realigning your business’s accounting year with the tax year. The 2023/24 tax year is a transitional year, so in order to get the profits aligned for 2024/25, more profit may fall in the 2023/24 tax year than you were expecting, resulting in a higher tax bill.

The example above shows that during the transitional year 2023/24 the self-employed person with a 31st May year end will be taxed on 22 months of profit, from 1/6/2022 to 31/3/2024. This will then bring you into line with the tax year in time for the change.

Will there be any relief to soften the blow?

Yes. You may have been in a similar situation when you started to trade. Your accountant may have explained to you that you had to pay tax on any ‘overlap’ profits which would be relieved when you ceased to trade or if your accounting period changes. These overlap profits have been stored up against the taxable profits from the transitional past.

Whatever your circumstances, it’s important that you talk to your accountant about the changes as soon as possible so you can be prepared for a possible larger tax bill. It’s crucial that you and your accountant find any overlap profits to relieve.

If you started trading many years ago, the information may not have been passed over if you had changed accountants, but all is not lost! Your accountant will be able to contact HMRC for the information. In certain circumstances, you may be able to spread the profits of the transitional period over the next five tax years. Your accountant can help you plan how to use your profits in the most tax efficient way. Make sure you understand the impact of this if you cease trading within those five years, as you may be liable to paying the whole amount owed in your final tax year.

Set aside time to do some additional tax planning with your accountant also. This may involve extra accountancy fees for you. Is it worth it? Absolutely. A plan could save you more in tax in the future.

What if I make a loss?

Normal losses are relieved in the current year against other income, carried back against profits of the previous year or carried forward to future years. If your accountant calculates a loss in the transitional period, then they may be able to carry a loss back three years.

What if I changed my accounting period end date to 31st March?

Changing your year-end date won’t make any difference to the amount of tax due. You’ll still have a spike in profits.

Your accountant might suggest you change your year end to 31st March from 2024/25 onwards, which will save you accountancy fees in the future. If you don’t move your year-end date to 31st March, pro rata profits will have to be calculated from two sets of accounts every tax year. In some circumstances if the second period of accounts are not yet completed, then your accountant may have to use estimates – more work involved as you will need to revise your tax return when your accounts are filed.

Are there any other impacts I should be aware of?

Here are the top three things to take into consideration:

Higher income in the Transitional year (2023/24)

If you earn between £50,000 and £60,000 you may be subject to the high-income child benefit charge (HIBC). This means the government will start to claw back any child benefit you or your partner received during the tax year. However, the Transitional part of the profit will not be included in the Net adjusted profit when assessing your income in relation to HIBC.

The impact on your pension

When deciding how much to contribute to your pension, you should always seek advice from your Independent Financial Adviser (IFA). If your net adjusted income is above a certain threshold, then the annual allowance may be tapered, which means you may have to pay a tax charge on contributions made above the annual allowance. However, the transitional part of the profits will not be included in the calculation of the net adjusted profit used to assess whether the annual allowance should be tapered.

Personal allowance

Normally, if your profits are over £100,000, your personal allowance is reduced by £1 for every additional £2 earned. This means that, when your profits reach £125, 140 you lose your personal allowance entirely. Unfortunately, transitional profits are included in that calculation for 2023/24

The most important message to take home here is to talk to your accountant. The rules are complex and planning ahead with a professional means you will be ready for any financial changes.

If you would like someone to demystify Making Tax Digital, and to start planning now, give us a call. We’d be delighted to talk to you.